When it Comes to Investing, Less is More

Quarterly NewsletterBy Dr. Robert Votruba

Avoidance and procrastination are natural enemies of goal achievement. To put off to tomorrow, what can be done today is a surefire way never to complete those nagging household chores, finally read that book your friend recommended last year, or cross the finish line feeling strong at a local 5k race. But, according to Nobel prize winner Richard Thaler, these same impediments to accomplishment could make you a better investor.

Dr. Thaler and colleague Dr. Shlomo Benartzi combine the disciplines of economics and psychology, referred to as Behavioral Economics, to study investor performance. A theory they developed, Myopic Loss Aversion (MLA), begins with the not-so-novel assumption that investors hate to lose money. Their research discovered that people feel more stress on days when the market is down and comparatively less relief on up days, and they overreact to losses.

Unfortunately, temporary losses are a normal part of investing. Consider: since 1925, the S&P 500 has averaged nearly 10% per year, yet almost 50% of the time it was down on any given day. So, for those checking their balances daily, the likelihood of seeing losses is the same as a coin flip.

Field experiments studying MLA found that individuals who receive information too frequently tend to underperform those who check their balances less often. The study found that “the investors who got the most frequent feedback (and thus the most information) took the least risk and earned the least money.” An investor who checks his or her investment portfolio quarterly instead of daily reduces the chance of seeing a moderate loss (of -2% or more) from 25% to 12%. Simply put, the less an investor sees short-term losses, the more likely they will stick to their long-term plan.

Of course, looking at our balances is easier than ever with online access and mobile apps. And avoiding financial newsfeeds is nearly impossible. Consider some of the following headlines from the first half of this year:

“What to expect as the US nears unthinkable debt default” – Financial Times

“Why everyone thinks a recession is coming in 2023” – CNBC

“The banking crisis will tilt the US into recession, say Fed economists” – CNN

“Could the US dollar collapse?” - Forbes

Yet, despite threats of recession, a bitter partisan battle over the debt ceiling, a series of bank failures, and the Federal Reserve’s ongoing battle with inflation, stocks (as measured by the S&P 500) had their best first half since 2019. Bonds, coming off their worst year ever in 2022, have also rebounded nicely. Yes, investors with diversified portfolios who did nothing rather than react to the headlines fared well during this year’s first six months.

A recession has been discussed as a near certainty for our economy for the past year. Recession forecasts by professional economists hit an all-time high late last year. A New York Fed recession model gives a 71% likelihood of a recession in the next 12 months. The most ominous sign that most economists point to is the inverted yield curve, a condition created when short-term interest rates are higher than long-term rates. Under normal circumstances, investors must be compensated better to tie their money up for longer, so a 10-year bond will usually offer a higher yield than one that matures in 3 months. But today, a 3-month treasury bill yields over 1% more than a 10-year treasury bond, indicating that investors believe the economy will weaken and the Fed will eventually have to lower interest rates. While inverted yield curves have preceded every recession since the 1950s, not all inverted curves have led to recession. Furthermore, the inverted yield curve does not indicate what type of recession is coming (short and shallow versus longer and deeper). Paradoxically, recessions have not meant doom for investors – on average, the S&P 500 has been in positive territory 12 months after a recession and up 33.4% three years after. This is especially true when the recession is widely expected as one is today (because it may already be “priced into the market”).

For years, Warren Buffet has advised investors not to bet against America, and this year was no different as he declared, “I have yet to see a time when it made sense to make a long-term bet against America.” So, while the resilience of the US economy in 2023 may not have surprised Mr. Buffet, it certainly caught those economists calling for recession off guard.

Despite some high-profile corporate layoffs, the labor market remains strong, with unemployment hovering near 50-year lows. As of the end of April, there were 10.1 million job openings in the US. Even though that is down from a peak of 12 million in March of 2022, it is still far above its pre-pandemic high of 7.2 million in January 2020. If, going forward, job openings continued to fall at the same pace as they have over the past 13 months, it would take until the end of 2024 to reach January 2020 levels. Given that over 68% of our economy is fueled by consumer spending, it’s hard to see a long and deep recession while we are at or near “full employment.” The following graph illustrates the long-term unemployment rate, accompanied by wage growth—the recent decline in wage growth is important in the Fed’s efforts to combat inflation.

While still elevated, inflation has been trending in the right direction (see chart below). Since peaking at 9.1% last year, the Consumer Price Index (CPI), the most common way to measure inflation, registered at 4% in May, well below April’s figure (4.9%) and its lowest annual increase in over two years. Lower energy prices (remember, last summer gas was running $5 per gallon), fewer supply chain disruptions, and the lagging impact of rising interest rates have all brought inflation back down toward historical averages.

Though the Federal Reserve acknowledges that there is still work to do in the fight against inflation, they finally paused in June after ten consecutive increases in interest rates. While 12 of 18 Federal Open Market Committee members expect at least two more .25% rate hikes before the end of the year, most agree that the vast majority of the rate hikes are behind us. Some market participants even expect rate cuts later this year or early in 2024. When presented with the highly variable nature of inflation figures and the once in a generation economic shock of COVID, we feel that forecasting interest rates several months out is a fool’s errand. Given that the S&P has returned 16.9% on average in the 12 months following the last interest rate hike of a cycle, the Fed’s last action is eagerly awaited.

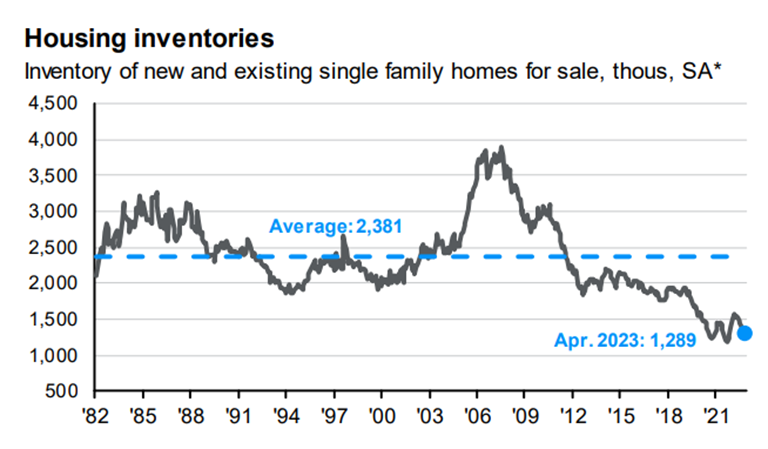

In addition to a strong job market and cooling inflation, the residential housing market's strength has also helped steer the economy from recession. Yes, many office buildings and regional malls remain half-empty. Still, given the historical spike in interest rates, most economic models would have also called for a dip in residential home prices. However, with fewer homes on the market (see chart), homeowners have benefited from a “wealth effect” created by rising prices.

Combined, these forces call into question whether a recession is such a certainty. Today, some headlines read:

“The case for a 2023 US recession is crumbling” – CNN

“Remember that looming recession? Not happening, some economists say” – CBS

“The U.S. isn’t in a recession – and it may not be headed for one” – MarketWatch

“Wall Street economists are increasingly less worried about a 2023 recession” – Yahoo!Finance

Using the last six months as a guide, it’s easy to see why Thaler and Benartzi’s behavioral theory was validated. At the turn of the year and throughout most of its first six months, investors would have been better off with less information. In Vanguard’s famous “Advisor’s Alpha” study, Vanguard attempted to quantify how much value an Investment Advisor can add to overall performance. Vanguard found that through various efforts, including spending strategy, asset allocation, and behavioral coaching, an Advisor can add “up to, or even exceeding 3% in net returns”. While this may sound self-serving, consider that Vanguard is a firm designed for do-it-yourself investors. So, if they have an inherent bias, it would be against Advisors. That aside, we wonder if Professor Thaler’s MLA theory is at play here. Maybe investors who employ an Investment Advisor seek less information about markets and the economy because they feel assured that someone else is watching for them, and as a result, perform better (up to 3%) than those without an Advisor. Perhaps Dr. Thaler could nudge his next doctoral candidate to consider this as a dissertation topic.

Registered Representative and Financial Advisor of Park Avenue Securities LLC (PAS). Securities products and advisory services offered through PAS, member FINRA, SIPC. Financial Representative of The Guardian Life Insurance Company of America® (Guardian), New York, NY. PAS is a wholly owned subsidiary of Guardian. National Financial Network is not an affiliate or subsidiary of PAS or

Guardian. CA Insurance License Number - 0D23495. Data and rates used were indicative of market conditions as of the date shown. Opinions, estimates, forecasts and statements of financial market trends are based on current market conditions and are subject to change without notice. References to specific securities, asset classes and financial markets are for illustrative purposes only and do not constitute a solicitation, offer, or recommendation to purchase or sell a security. Past performance is not a guarantee of future results. S&P 500 Index is a market index generally considered representative of the stock market as a whole. The index focuses on the large-cap segment of the U.S. equities market. Indices are unmanaged, and one cannot invest directly in an index. Past performance is not a guarantee of future results.

2023-158139 Exp 07/25